The information contained in this document is provided for general information purposes only, is not provided for decision making nor for use in design, and must not be relied on as specific advice in connection with any decisions the reader may make. Statements contained in this document that state Ascent Engineering Inc.’s expectations or predictions of the future are forward-looking statements intended to be covered by the safe harbor provisions of the Securities Act of 1933 and the Securities Exchange Act of 1934. The words “believe,” “estimate,” “expect,” “forecast,” “could,” “may,” “will,” “targeting,” “illustrative,” or other similar expressions identify forward-looking statements. It is important to note that actual results could differ materially from those projected in such forward-looking statements. No representations or warranties, express or implied, are made by Ascent concerning the applicability, suitability, accuracy, or completeness of the information contained herein and Ascent does not accept any responsibility whatsoever for the use of this information. Ascent is not liable for any action the reader may take as a result of relying on such material or for any loss or damage suffered as a result of taking this action.

Crude oil has been the foundation of modern civilization for over a hundred years, but the world appears to be at the precipice of a shift towards renewable energy, electrification, and CO2 reduction. From transportation fuels to plastics to household cleansers and cosmetics, petroleum products are an essential part of everyday life. In recent years, however, the world has begun moving towards electrification and renewable energy and has seen significant changes in attitudes towards carbon consumption and greenhouse gas (GHG) emissions. Electrification is evidenced by the growth of Tesla into the largest automobile manufacturer with a market capitalization equal to the next nine largest automobile manufacturers combined. Virtually all automobile manufacturers have committed to electrification. Big name companies in the oil industry such as ExxonMobil, Shell, and ConocoPhilips have issued statements regarding sustainability and plans for reduced GHG emissions in the future. Many countries have targeted carbon neutrality by 20501 and have issued government mandates to achieve this. But even if every new car were to be electric by 2030, which is beyond even the most forward plans, there will be over a billion existing internal combustion engine vehicles operating for the foreseeable future. Renewable liquid fuels provide a transition fuel until electrification is completed. This changing energy landscape presents opportunities both for refiners who are already established in the oil and gas industry to produce renewable fuels as well as for entrepreneurs with emerging renewable processes to gain a foothold in the age of renewable energy. Ascent Engineering has a well established history of expertise in successful and innovative refinery retrofits and is also well positioned to help new renewable processes make the transition from the laboratory to commercialization.

It is hard to imagine modern civilization today without the contributions from crude oil. In 2019, crude oil supplied 33% of the world’s energy with the balance from coal (27%), gas (24%), and non fossil fuels (16%) including solar/wind/hydro, biofuels, and nuclear.2 Only about 10% of global energy is renewably sourced. Petroleum based gasoline, diesel, and jet fuel are the primary energy sources for transportation. As the world looks to reduce emissions, renewable fuel options include utilizing sustainable feedstocks to source transportation fuel or making a switch to electric vehicles. While electric vehicles are gaining traction in the United States and the world, the global generation of electricity is still heavily coal based and is not currently a carbon neutral energy source. With over 280 million cars, trucks, busses, and motorcycles on the road in the U.S. alone,3 there is a large installed base of internal combustion engine (ICE) vehicles that can see reduced CO2 emissions in the near term by incorporating renewably sourced liquid transportation fuels, even if electric vehicles are the future. Until the worldwide electrical grid is made to be less carbon intensive, renewable liquid fuels can produce less CO2 than an electric vehicle relying on the existing electrical grid utilizing high carbon sources such as coal. With mandates and government incentives, producing alternative liquid fuels can be a profitable way for existing refiners to effectively revamp their existing assets, and also for new technologies to produce alternative liquid fuels.

Carbon dioxide (CO2) is the primary component in greenhouse gas emissions from transportation fuels, although methane (CH4) is more potent in its ability to trap heat. There are other pollutants in vehicle emissions such as particulate matter, volatile organic compounds (VOCs), nitrogen oxides (NOx), carbon monoxide (CO), and sulfur dioxide (SO2). According to the U.S. Environmental Protection Agency (EPA), the transportation sector is the largest producer of greenhouse gases in the U.S.

The United States has a “Statement of Intent” to be carbon neutral by 2050,1 meaning carbon dioxide output is to have a net neutral impact to the environment. Since all fossil fuels are carbon based, they will always produce CO2 upon combustion and are therefore incompatible with this intent. Carbon capture and sequestration (CCS) can be used to reduce CO2 emissions at the source, and some producers are planting trees to offset some of the carbon emissions. However, to fully meet the intent, the U.S. will need to invest heavily in renewable energy.

Emissions are considered “well-to-wheel”, that is at every step along the way from sourcing the feedstock, processing it into transport fuel, and consumption in the vehicle. Oil and gas companies can become carbon neutral for direct emissions from company operations and indirect emissions from consumed energy.4 Carbon intensity (amount of carbon by weight emitted per unit of energy consumed5) of petroleum-based products can be reduced by mixing biologically made renewable fuels with the petroleum fuels. The feedstocks for renewable fuels include various plants and animal fats. Blue hydrogen (produced from petroleum-based sources, but the carbon is captured and sequestered) or green hydrogen (produced entirely from non-petroleum-based sources) can be used for refinery hydroprocessing.

Renewable fuels facilities can be incorporated into existing refinery facilities. A refiner may consider a retrofit to existing hydroprocessing facilities to process renewable feedstocks into renewable fuels. It is possible and economically advantageous with government credits to process the renewable fuels in a mixture with petroleum-based fuels. Incorporating the use of green sources of energy such as wind or solar or re use of waste gases for the production of the petroleum-based fuel uses renewable energy in the existing transportation fleet.

A knowledgeable engineering firm can work with owners and licensors to deliver process units capable of meeting the renewable fuels requirements. Ascent Engineering is ideally positioned to evaluate existing equipment for retrofit as well as new processes and to strike the balance between the licensor’s requirements and the refiner’s existing assets.

Humans have always aimed to advance the latest technology and automobiles are no exception to the rule. While steam was the earliest automobile fuel of choice, by the mid to late 19th century, steam was all but forgotten and it remained to be seen whether gasoline or electric would rule the industry. Gasoline powered vehicles were noisy, dirty, and difficult to start due to a hand crank. Electric vehicles were silent, clean, and provided an instant start, but there was insufficient infrastructure for charging batteries. The charging problem was solved with widespread availability of electricity at the turn of the century; however, electric cars simply could not compete with the range provided by a gasoline powered car. Additionally, gasoline was cheap and efficient, and suddenly the automotive industry found itself on the path of fossil fuels.6

Now, more than a century later, the world of transportation fuels is seeing the next big transformation. Government mandates to reduce carbon emissions, improved battery technologies allowing further range, and sustainable feedstocks for use in the existing fleet are changing the future fleet’s fuel mix. Technology is being developed to process a widening assortment of sustainable feedstocks and to discover different pathways to create the renewable energy sources. The large base of existing ICE vehicles on the road represent a huge consumer pool for renewably sourced fuels as a way to reduce emissions for the duration of these vehicles’ serviceable lives.

The energy rich liquid which is commonly known as gasoline has evolved over the last century and a half. The light liquid, historically produced by distilling crude oil, was initially disposed of as a waste product. It was a necessary waste to retrieve the precious kerosene. The heavy liquid which was left after recovering kerosene was also disposed of as waste. Technological advances have led to major improvements in the quality and quantity of gasoline. With the focus on renewable feedstocks for liquid fuel production, it is key for the technology to maintain modern standards for gasoline performance and fuel efficiency. Ascent can help guide a refiner to optimize their plant configuration to achieve this.

The invention of the automobile in 1892 along with gasoline’s high efficiency as a fuel source led to gasoline becoming a valuable fuel. Increasing automobile numbers increased the demand for gasoline supply. Concurrently, electrification of lighting reduced the demand for kerosene. The problem of gasoline undersupply and kerosene oversupply was solved with the development of thermal cracking. The heavier portion of crude was cracked into gasoline range material. The cracked gasoline was blended with the straight run gasoline. Light and heavy liquids were blended to achieve the desired density of gasoline.

Gasolines from different crudes along with blending of cracked gasolines led to wide variations in the performance of automobile and aviation engines. Since crude compositions vary widely, the quality of the straight run gasolines also varied widely. Early gasoline was rated based on Baume scale and volatility.

Abnormal combustion is a phenomenon where the gasoline vapor burns by heat and compression prior to the spark from the spark plug. This pre-ignition can lead to hot running engines with reduced power and potential damage due to “knock”. Different gasolines have different resistance to abnormal combustion. Aromatic and naphthenic gasolines, with their higher octanes, have higher resistance to knock than paraffinic gasolines.

Until 1929, there was no consistent standard for gasoline quality. In 1929, the octane rating scale was adopted. Octane is a measure of how much compression gasoline can withstand before igniting. A higher octane number can handle higher compression and is less likely to suffer pre-ignition. Octane of gasoline is measured against a mixture of iso octane (2,2,4-trimethylpentane) and n heptane. Iso octane is assigned an octane number of 100 while n heptane is assigned an octane number of 0. The octane of gasoline is measured by running it in a test engine with variable compression ratio. The test results are compared to mixtures of iso octane and n heptane. RON is the Research Octane Number and is determined by running the fuel in a test engine at idle conditions. MON is the Motor Octane Number and is determined by running the fuel in a test engine at higher speeds and temperatures. The octane number reported at the gas pump is the average of the two, or (R+M)/2.

Air quality became a concern as industrialization released pollutants into the atmosphere. Ambient air quality in the United States was regulated by congress and the U.S. Environmental Protection Agency (EPA) was formed in 1970 to provide consistent national guidelines for protecting the environment, as well as to monitor and enforce the subsequent regulations. In the same year that the EPA was founded, the Clean Air Act was passed which, among other responsibilities, allowed the EPA to regulate emissions from light duty vehicles. Later, amendments were passed to the Clean Air Act to introduce stricter emissions regulations. For gasoline-powered automobiles, the biggest U.S. national impact came in the form of Reformulated Gasoline (RFG) program (passed in 1990, phased in 1995-1999), Tier 2 (passed in 1999, phased in 2004 2009), and particularly the current Tier 3 regulations for emissions from light duty vehicles passed in 2014 and phased in 2017-2025.7 The RFG program was aimed at overall smog reduction (VOCs, NOx, and toxic pollutants) by mandating oxygenate blending through two phases of emission restrictions. The Tier 2 Gasoline Sulfur program imposed a restriction on sulfur levels to 30 ppmw by 2006 (though some small refiners had some leniency to an 80 ppmw cap). The Tier 3 Gasoline Sulfur program imposed a tighter restriction on sulfur levels to 10 ppmw. Ascent has successfully worked with various clients to achieve Tier 3 compliance.

As gasoline technology has progressed and as regulations have changed, various additives have been included in gasoline blendstocks to increase performance and reduce emissions. Many of these are oxygenates, or oxygen bearing compounds which promote combustion. The addition of oxygenates reduces carbon monoxide in the exhaust. Use of such oxygenate blends came to prominence in the 1970s partly as a result of the oil embargo driving up oil prices; domestically sourced additives helped to reduce U.S. need for foreign oil and was more environmentally friendly as well.

TEL:

Tetraethyllead (TEL) was used for many years to increase the octane of gasoline. The increased octane using TEL allowed the development of more efficient engines with higher compression ratios. Unfortunately, TEL is toxic and the effects of lead poisoning in children and emissions to the environment were the primary reasons for the phase out. Worldwide, TEL phase out from road gasoline began in the 1970s. Japan was an early adopter of unleaded gasoline and stopped using leaded gasoline by 1980. Many other countries such as Canada and much of Europe had completed TEL phase out by the mid-1990s including the United States by 1996.8

MTBE:

MTBE (Methyl tertiary-butyl ether) was introduced as an oxygenate to improve combustion and reduce tail pipe emissions. The miscibility of MTBE with ground water has caused its use to be discontinued in the U.S. MTBE can be tasted in water at very low concentrations. Health risks associated with MTBE have not been quantified, but it is believed to be a human carcinogen.

Ethanol:

Ethanol has been around for well over a hundred years as a fuel source and its use as a gasoline additive has waxed and waned over the years as driven by wartime needs and taxes.9 Ethanol is a high octane oxygenate as well as a renewable energy source. The production and consumption of ethanol is part of the renewable energy requirement in today’s regulatory environment and it is by far the largest volume of renewable fuel stock in the United States.

Automobile fuel economy requirements are driving improvements in engine efficiency. The current U.S. federal Corporate Average Fuel Economy (CAFE) requirement is that the industry fleet wide average mileage for cars and light duty trucks be 40.4 mpg by 2026.10 On the manufacturing side, the industry is trending towards smaller engines. The smaller displacement (as well as reduced weight) help improve fuel economy, while modern technology can exact as much or more power from the smaller displacement engines. On the fuel side, automobile manufacturers such as General Motors are asking for improvements in fuel performance in order to help maximize engine efficiency. This would include higher octane fuel with higher RON and higher sensitivity (RON-MON). In lay terms, higher sensitivity means more stability at low temperatures and faster reactions at high temperatures to allow for high compression engines.11

Ethanol:

As mentioned above, ethanol is commonly blended into gasoline as an oxygenate to reduce emissions. It can be produced from any number of renewable feedstock sources. In the U.S., ethanol is commonly produced from corn. Because ethanol counts as renewable fuel and is already so readily available, there is incentive to use more of it in gasoline blends. The most common ethanol blend contains up to 10% ethanol (E10), although in 2011 the EPA allowed use of up to 15% ethanol (E15) in automobile models from 2001. Gasoline with 85% ethanol (E85) is also available for automobiles which are specifically designed for it (flex fuel). Because ethanol is such a good solvent, specially designed fuel injection systems are required to prevent corrosion. Additionally, because ethanol has an oxygen atom, therefore it is a partially oxidized hydrocarbon, it contains less energy upon combustion than a non-oxygenated hydrocarbon. E10 gasoline typically has a 3 to 4% lower fuel mileage than 100% gasoline. E15 gasoline mileage is typically 4 to 5% lower than 100% gasoline. E85 gasoline can have 51 to 83% ethanol and 15 to 27% lower mileage.12

Diesel is a crude oil fraction named after the inventor of the diesel engine, Rudolf Diesel. Rudolf Diesel sought to develop an engine with 100% efficiency. In his attempts to achieve this, he increased the compression ratio. Unlike spark ignited engines, diesel engines rely on the high temperature of the compressed air to ignite the fuel once it is injected into the cylinder under pressure. Since the fuel is not compressed as a mixture with air, it does not have the problem of preignition that gasoline engines have. The compressed air in a diesel engine reaches temperatures above the autoignition temperature of the fuel. When the fuel is injected into the hot compressed air cylinder, it ignites, causing the power stroke of the cylinder. By having very high compression ratios relative to gasoline engines, much higher fuel efficiency can be achieved. Diesel also produces more power per gallon because of its higher density than gasoline. During his lifetime, Diesel achieved engine efficiencies over twice that of gasoline engines.

Diesel engine efficiency has historically made diesel engines the engine of choice for industry and in Europe. Diesel has higher energy content per unit volume than gasoline. This is principally due to the density difference. Gasoline density varies from 45 to 49 lb/ft3 (721 to 785 kg/m3) while diesel density varies from 51 to 60 lb/ft3 (817 to 961 kg/m3). Since the heating value of all hydrocarbons is roughly 20,000 BTU/lb (46,500 kJ/kg), the higher diesel density translates to higher energy content. Diesel has roughly 10 to 15% more energy than gasoline on a per volume basis.13

The higher diesel energy content and engine efficiency compared to gasoline engines yields higher fuel mileage. Because diesel engines do not use a spark ignition to combust the compressed air and fuel mixture, they do not suffer from pre-ignition. This allows diesel engines to be designed for much higher compression ratios (14 to 22) than gasoline engines (8-11). Modern truck diesel engines can achieve 40 to 47% efficiency versus spark-ignition engine efficiency at 30-36%.14

In the United States, the allowable sulfur content in diesel fuel was reduced to 500 ppm in 1993. Prior to that, diesel sulfur content could be as high as 5,000 ppm. This low sulfur diesel was introduced to reduce sulfate particulate emissions. Hydrotreating is the primary means of reducing sulfur in diesel.

Ultra low sulfur diesel (ULSD – 15 ppm) was phased in beginning in 2006. After 2010, the EPA required that all diesel supplied to the U.S. market be ULSD and that all diesel vehicles use ULSD.15 The lower sulfur content requires more severe hydrotreating.

Like octane for gasoline, cetane number is a measure of diesel fuel performance. Cetane number is an indicator of a fuel’s ignition characteristics, specifically a measure of ignition delay after injection into the cylinder. A higher cetane number is indicative of less ignition delay, which translates to better engine performance. Cetane number is determined by a test performed on a standard single cylinder, variable compression ratio, diesel engine and comparing the fuel against a mixture of cetane (cetane number = 100) and heptamethylnonane (cetane number = 15). In order to avoid testing every fuel, cetane index was developed as a calculated approximation of a fuel’s cetane number. The cetane number measured by cetane index is calculated by a formula using a fuel’s density and distillation range according to American Society for Testing and Materials (ASTM) D-86 T10, T50, and T90.16 The calculated cetane index is +/-2 numbers from the cetane number.

Conventional Diesel, Biodiesel, Renewable Diesel, and the Future

While electrification has begun replacing gasoline, electrification has made lesser inroads to date in the higher energy demand industrial diesel market. Newly emerging electric semi trucks struggle with range per charge and long charging times as well as large battery size, which result in longer travel times and smaller loads (if competing for space with the large battery). Large scale use of heavy duty electric vehicles is still a number of years away. Renewable diesel produces less CO2 than conventional diesel while providing the same high energy density required for heavy duty transport until electric technology catches up. Renewable diesel is cleaner burning than its conventional or biodiesel counterparts in addition to having a better cetane number for higher performance.

It is important to note that there are a number of terms surrounding diesel fuel that oftentimes get confused. Conventional diesel is traditional, petroleum-based diesel that is made from crude oil in an oil refinery. Biodiesel is not sourced from fossil fuels; rather it comes from renewable sources such as vegetable oils or animal fats. It is produced by a process called transesterification, or reaction of a glyceride and an alcohol (usually methanol) to make biodiesel (fatty esters) and glycerol. Biodiesel properties differ from conventional diesel in that biodiesel solidifies at cold temperatures, may separate during storage, and most importantly, the chemical structure differs enough that biodiesel cannot be used as a stand-alone substitute for conventional diesel fuel – it must be blended prior to use in traditional diesel engines. Finally, while renewable diesel is sourced from the same feedstocks as biodiesel, the process to produce it is more like that of conventional diesel. Because renewable diesel sees the same hydrotreating processes as conventional diesel, it has the same chemical structure as conventional diesel and can be used without blending. Renewable diesel does not contain oxygen and thus does not have the same cold and storage issues as biodiesel.

There are two main government renewable fuel incentive programs that are currently differentiated on a national and state level in the United States.

The Renewable Fuel Standard (RFS) is set by the Environmental Protection Agency (EPA) on the national level.

Any of a number of carbon fuels programs adopted on the state government level. Current programs in effect and other state progress as of Q2 2021 include the following:

California – Low Carbon Fuels Standard (LCFS) – currently in effect

Oregon – Clean Fuels Program (CFP) – currently in effect

Colorado – GHG Reduction Roadmap has been established, but its feasibility study on carbon fuels program concluded not to adopt. Instead, a zero emission vehicle mandate is part of the roadmap.

Utah – Air Quality Roadmap has been established, but acts as a loose guideline with no call out of a carbon fuels program. Zero emission vehicle focus is called out in the roadmap.

New York – State Senate Bill S2962A establishes the Clean Fuel Standard and is in committee.

Washington – State House Bill 1091 establishes the Clean Fuel Standard and State Senate Bill 5126 establishes a carbon cap-and-trade program and both have passed through voting committee. The programs will be in effect January 2023 once signed by the governor.

Minnesota – State House Bill HF 2083 dubbed the “Future Fuels Act” was introduced in the Minnesota House of Representatives and referred to the House Committee on Commerce, Finance and Policy.

In addition, Canada has recently published proposed regulations for its Clean Fuel Standard, to be implemented nationwide, with final regulations to be published in 2021. The expected enforcement of the Clean Fuel Standard is at the end of 2022. As of 2021, British Columbia is the only province of Canada that has a carbon program in effect, known as the British Columbia’s Low Carbon Fuel Standard (BC-LCFS).

Unless otherwise noted, any reference to a low carbon fuels program in this text refers to the California LCFS program as they are the largest market for carbon credits.

The subtle difference between the federal RFS program and the California LCFS program is that the RFS program is aimed at directly setting renewable fuel volumes, driving the demand for the national bulk production and use of renewable fuels, with concomitant reduction in greenhouse gas (GHG) emissions. The LCFS program is aimed at directly setting carbon volumes, as opposed to renewable fuel volumes, and requires a more stringent carbon accounting in the life cycle of the final fuel product.

The RFS and LCFS programs financially impact refiners and importers of gasoline and/or diesel sourced from petroleum. Both of these programs are designed to incentivize renewable fuel production and carbon emission reduction. Both programs introduce a supply-and-demand market of credits. Both programs put petroleum-based refiners and importers into a deficit position, creating the “demand” of renewable fuel and carbon credits. The “supply” of the credits comes from entities that generate a renewable fuel with a proven pathway of reduced GHG emissions compared to petroleum-based fuels.

In the RFS program, refiners must either purchase credits (referred to as Renewable Identification Numbers, or RINs) or physically blend renewable fuels into their gasoline and diesel fuel pool to meet compliance. Furthermore, the RFS program requires four different categories of renewable fuels to blend as part of meeting compliance. These four categories include fuels derived from cellulosic, biomass, advanced, and renewable feedstocks.

In the LCFS program, the main focus is carbon emissions attributed to the life cycle pathway to generate gasoline and diesel. Every year, the California Air Resources Board (CARB) updates the CI (carbon intensity) scores of California fuels (CARBOB, or California Reformulated Gasoline Blendstock for Oxygenate Blending, and ULSD) and this sets the emissions life cycle of gasoline and diesel fuel sold in California, and for all obligated parties to which it is subject. The CI scores of these fuels are relatively high due to being sourced from carbon emitting intensive processes. The LCFS program sets a CI benchmark reduction target for these fuels, for which a delta in CI score between the higher CI fuel and lower CI benchmark exists, creating the deficit position and “demand” for credits. Entities that provide alternative fuels with a proven life cycle pathway CI score lower than the benchmark is the “supply” of credits to which obligated parties in a deficit position can purchase. CARB offers programs for obligated parties to consider in order to offset their deficit position.

The United States EPA has implemented a national RFS program which is the foundation of America’s renewable energy policy. This national policy is aimed at reducing oil imports and protecting the environment by reducing air pollution and greenhouse gas emissions. The RFS program has gone through a history of amendments and expansions dating back to its initial creation under the Energy Policy Act of 2005.17

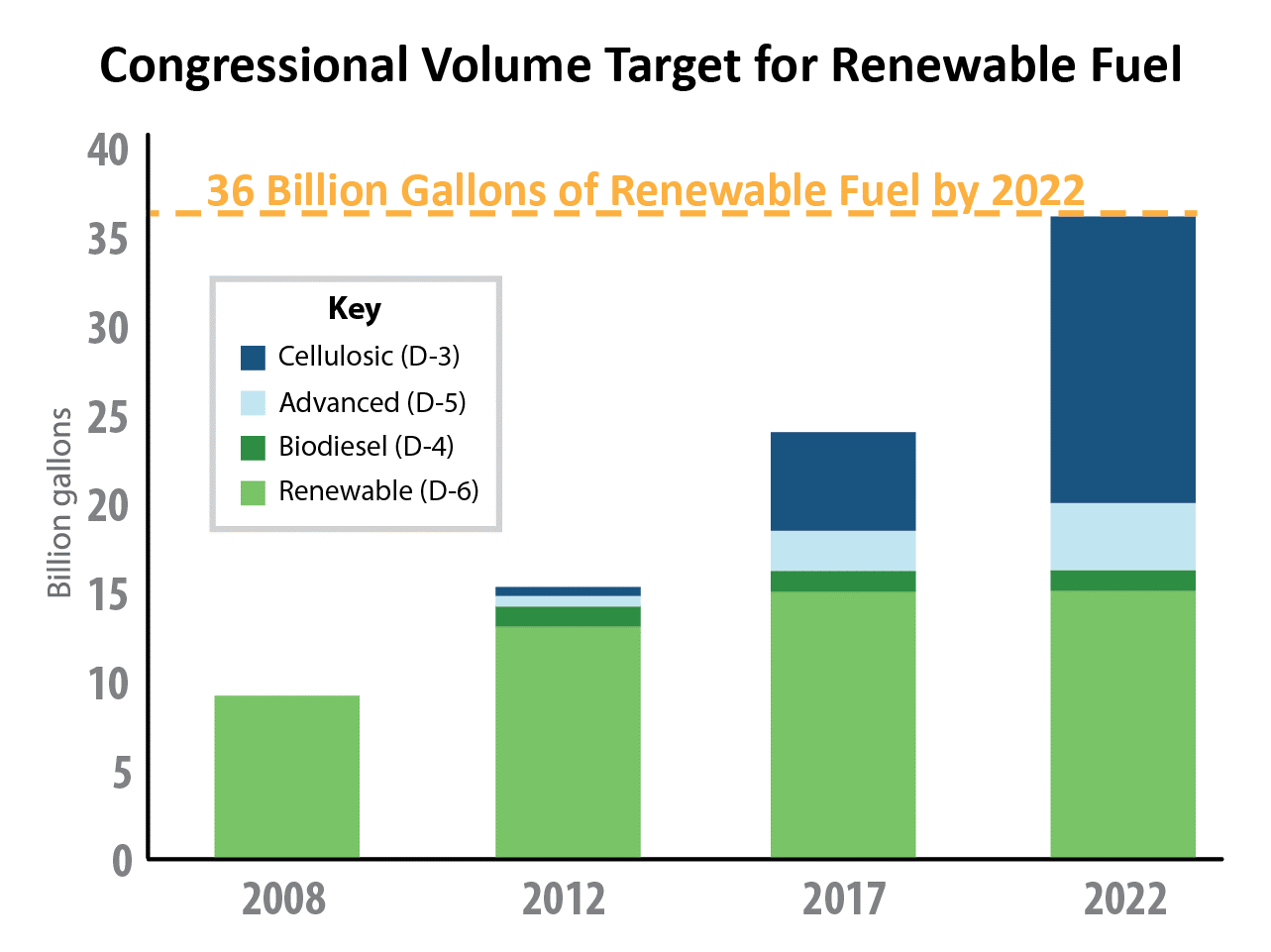

The RFS program is a national policy that requires a certain volume of renewable fuel to replace or reduce the quantity of petroleum-based transportation fuel. The Energy Independence and Security Act of 2007 (EISA) specifies the total RFS volume requirements through the year 2022. The long-term goal is 36 billion gallons annually (2.35 million BPCD or 11.2 million m3/m) of total renewable fuel by 2022. The law requires EPA to set RFS volumes for 2023 and beyond, according to certain criteria defined in the statute. Figure 1 below shows the RFS EPA congressional volume targets.18 The detailed tabulated values can be found on the EPA website.

Figure 1: RFS EPA Renewable Fuels Volume Targets

Obligated parties under the RFS program are refiners or importers of gasoline and/or diesel fuel. Based on the renewable fuels volume targets in the graph above, this sets a regulated party’s Renewable Volume Obligation (RVO), the deficit position. Compliance is achieved by blending renewable fuels into transportation fuel or by obtaining credits called Renewable Identification Numbers (RINs) to meet the EPA-specified RVO. To be explicit, the regulated party is obligated to blend and meet each of the four different types of renewable fuel targets into their fuel pool. The EPA sets the RVO requirement and refiners or importers must demonstrate compliance annually. For example, a transportation fuel sourced from 100% fossil fuel will not meet compliance. The refiner or importer must purchase a renewable fuel source under the RFS program with RINs attached and blend it into the transportation fuel to meet the annual RVO. It is also possible to purchase RINs as credits to meet compliance.

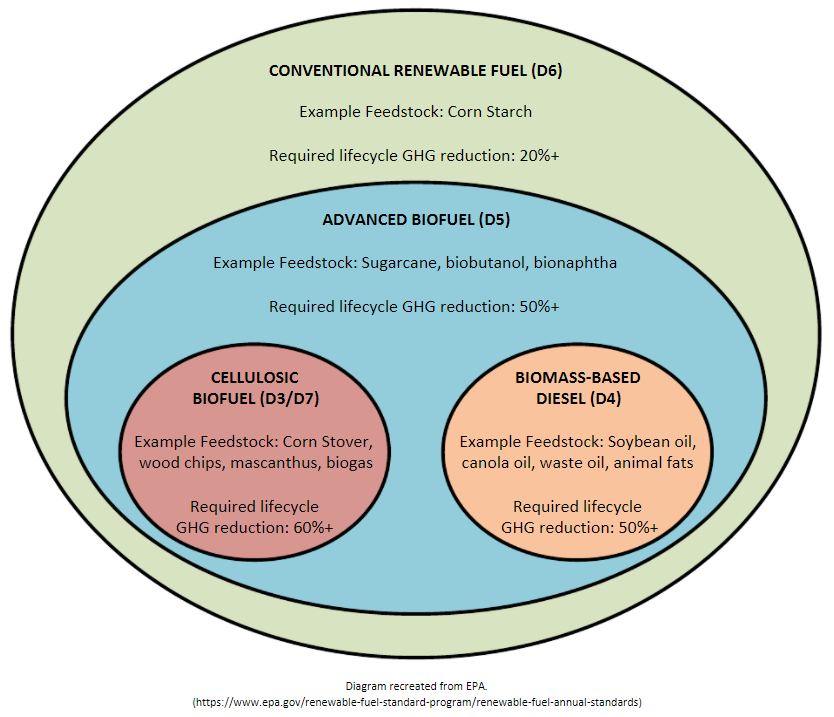

There are four different categories of renewable fuels that the RFS program mandates for obligated parties to blend into their fuel pool. The RVO for each of these four categories must be met for each compliance year. The four categories are essentially categorized by a combination of the feedstock and minimum GHG emission reduction requirement. The four categories and their accompanying RIN codes are as follows, arranged from more advanced RINs to less advanced RINs:

The four categories fit into a “nesting” structure, meaning more advanced RINs can be used for compliance of less advanced fuel categories. Figure 218 and Table 118 convey the same message of how each RIN code can be used for each fuel category, and also described below:

RIN codes D3 Cellulosic Biofuel and D7 Cellulosic Diesel can count for Advanced Biofuel and Renewable Fuel

RIN code D4 Biomass-based Diesel can count for Advanced Biofuel and Renewable Fuel

RIN code D5 Advanced Biofuel can count for Renewable Fuel

Unfortunately, cellulosic production of renewable fuels has not reached commercialization due in part to poor economics. Lack of cellulosic renewable fuels production has led the EPA to sell credits to the industry to satisfy this RIN obligation.

More RINs can be generated from higher energy content fuel compared to ethanol as the base fuel. A single RIN has the energy equivalency as 1 gallon of ethanol, hence renewable fuels with higher energy content than ethanol can generate more than 1 RIN per gallon. For example, biodiesel can generate 1.5 RIN, renewable diesel can generate 1.7 RIN, and butanol can generate 1.3 RIN.

Figure 2: Fuel Nesting Scheme for RFS Program

Table 1: D-Code Compliance to the Four Fuel Categories

D-Code

Cellulosic Biofuel

Biomass-Based Diesel

Advanced Biofuel

Total Renewable Fuel

3

X

X

X

4

X

X

X

5

X

X

6

X

7

X

X

X

For a renewable fuel to qualify under the RFS program and generate RINs, a petition must be submitted to EPA for review and approval. The critical assessment of the renewable fuel is the lifecycle greenhouse gas emissions analysis, and it must demonstrate a reduction in GHG emissions compared to a 2005 petroleum baseline. EPA's lifecycle analysis for the RFS includes emissions related to:

All sources of carbon emissions are considered as part of a GHG life cycle pathway for any transportation fuel, which also includes grid electricity. The majority of the U.S. produces grid electricity by carbon emitting processes. A renewable fuels facility that powers process equipment from carbon-sourced grid electricity will still have a GHG emission footprint. A renewable fuels facility has lower life cycle GHG emissions than a petroleum based facility, but can still be better improved by sourcing electricity from zero emission sources. Consuming renewable fuels is a first overall step in reducing GHG emissions in the transportation sector for existing internal combustion engines. Utilizing renewable electricity minimizes the GHG footprint of renewable fuels and is a step towards electrifying the existing ICE fleet without total fleet replacement. Transitioning the grid electricity to zero emission sourced, combined with adoption of electric vehicles, would be the second step to achieve near zero carbon emission in the transportation sector.

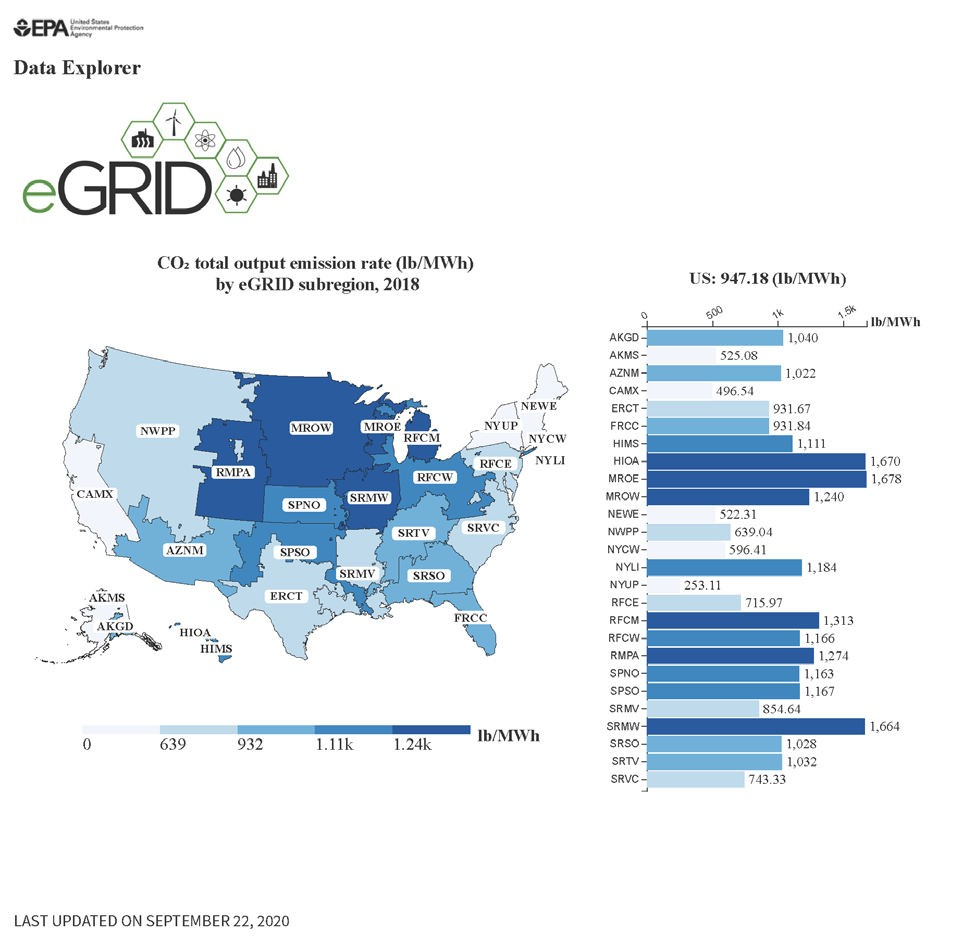

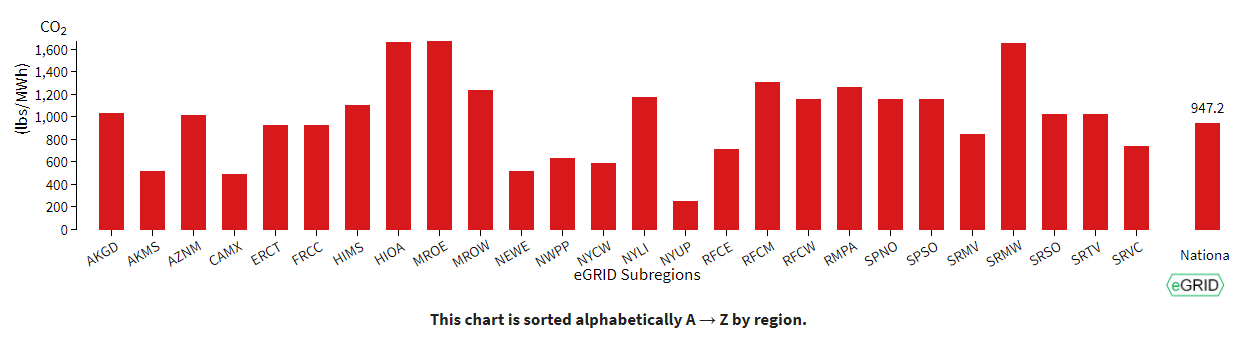

Specific only to the RFS program, the lifecycle GHG analysis uses the EPA Emissions & Generation Resource Integrated Database (eGRID), where the U.S. is divided into electrical grid regions. Electricity emission factors are an average grid basis that includes the mix of various electricity generation sources. The eGRID is a comprehensive source of data on the environmental characteristics of almost all electric power generated in the United States and is updated periodically. Figure 3 below depicts the eGRID subregions of the U.S. and provides the corresponding CO2 emitted based on the source profile mix. The following Figure 4 and Figure 5 depict a breakdown of the electricity source profile of each region and the corresponding average CO2 emissions.

The eGRID data presented here highlight the fact that the majority of the U.S. electrical grids are currently powered by carbon based sources. California is typically touted to be the green initiative state, and with nearly 50% of the electricity generation powered by natural gas, it has one of the lowest carbon emission rates in the nation. A majority of other U.S. regions have electricity generation portfolios with higher exposure to fossil fuels. From the standpoint of achieving nationwide net zero carbon emissions, a significant overhaul in the U.S. electrical infrastructure is required to support lower CO2 emissions for general electrical use and for transportation use in electric vehicles. Renewable fuels are an interim pathway to achieve lower CO2 emissions for the existing internal combustion engine fleet.

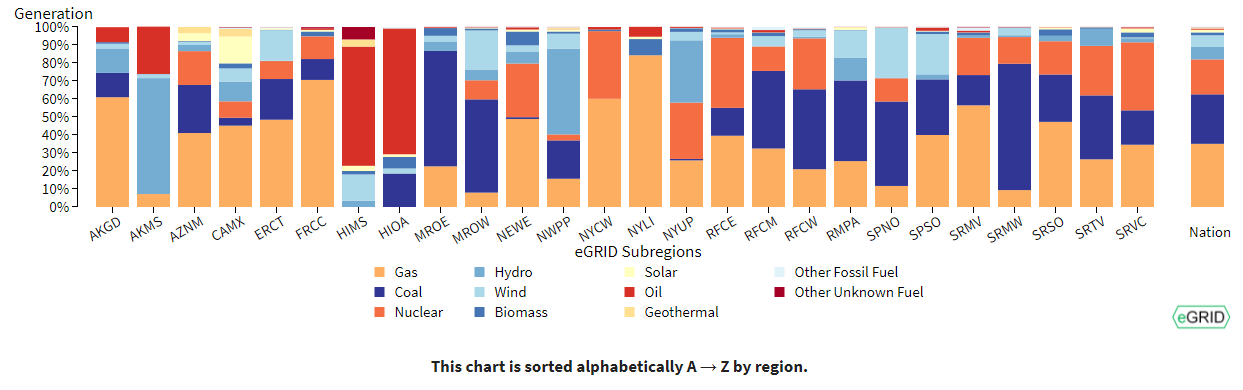

Figure 3: eGRID Subregion Map and Average CO2 Emission RatesFigure 4: Fuel Mix or Sources Used in Electricity Generation

Fuel Mix: This chart compares fuel mix (%) of sources used to generate electricity in all eGRID subregions.Figure 5: CO2 Average Emission Rates

Emission Rates: This chart compares the average emission rates in pounds per MWh in all eGRID subregions to the national average emission rates for CO2.

The LCFS program is designed to decrease the carbon intensity (CI) of transportation fuels pool by providing a mechanism to introduce a range of low carbon and renewable fuel alternatives. The result is a lower carbon footprint for the fuel being consumed. The importance to renewable fuel is the production tax incentives. These will be discussed later but the economics of renewable fuels are LCFS driven.

The carbon intensity is a metric used to measure the carbon emitted per unit of energy consumed throughout the life cycle pathway of a fuel source. Note that the CI score referenced under LCFS program (typically in units of gCO2e/MJ) can be loosely compared to the RFS lifecycle GHG analysis results (typically in units of kgCO2e/MMBtu), but both are calculated by different methodologies.

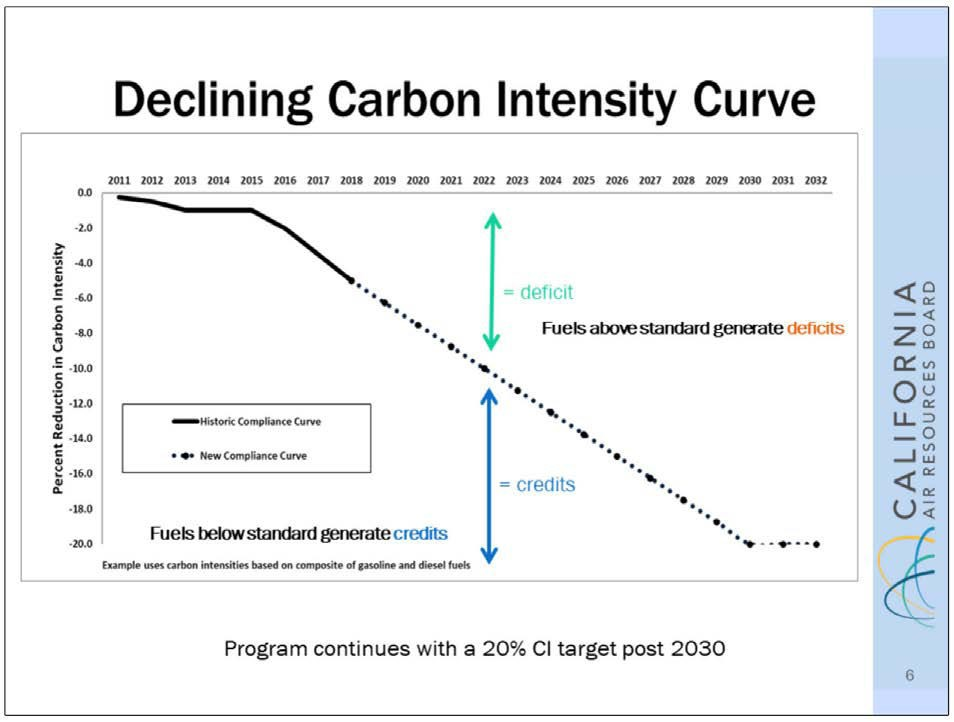

Carbon intensity is important to regulated parties because CARB establishes annual CI benchmarks for the transportation fuel pool, specifically gasoline and diesel. There is a planned schedule of CI reduction of California’s transportation fuel pool to 2030 and beyond. Regulated parties include fuel importers, refiners, and wholesalers who are required to reduce CI score across their transportation fuel product line. To ensure that the overall California transportation fuel pool meets the annual LCFS CI benchmark target, a regulated entity must lower the CI of its fuel pool (by substituting cleaner fuels) and/or purchase LCFS credits from other regulated entities. LCFS credits do not expire and any surplus of LCFS credits can be banked for future compliance.5

Figure 6 below depicts the overall reduction of the CI benchmark through 2030 and beyond and simplifies the supply/demand interaction of LCFS credits. A regulated party of transportation fuels with deficits must generate or acquire enough credits to be in annual compliance with the standard. Other entities, such as biofuel refiners, electricity, and natural gas suppliers can opt into the program to generate valuable credits so long as the CI pathway for those fuels are lower than the standard.

Figure 6: California LCFS CI Benchmark and Deficit/Credit

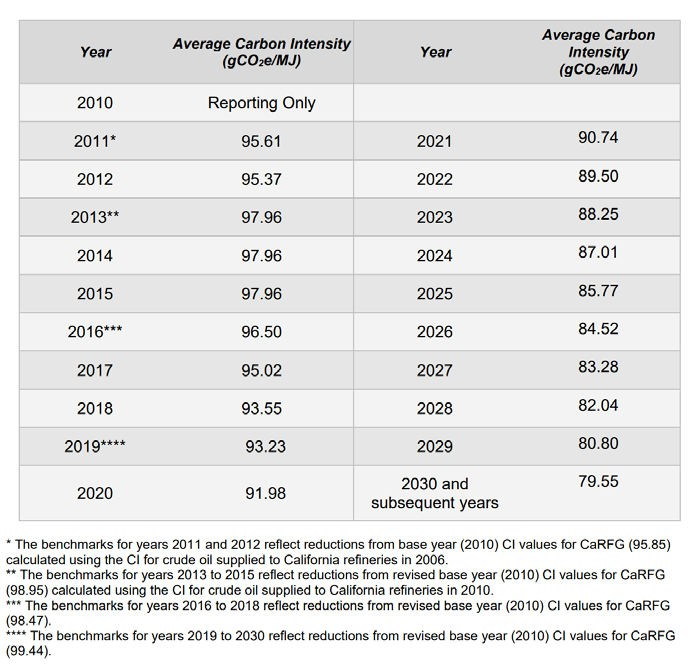

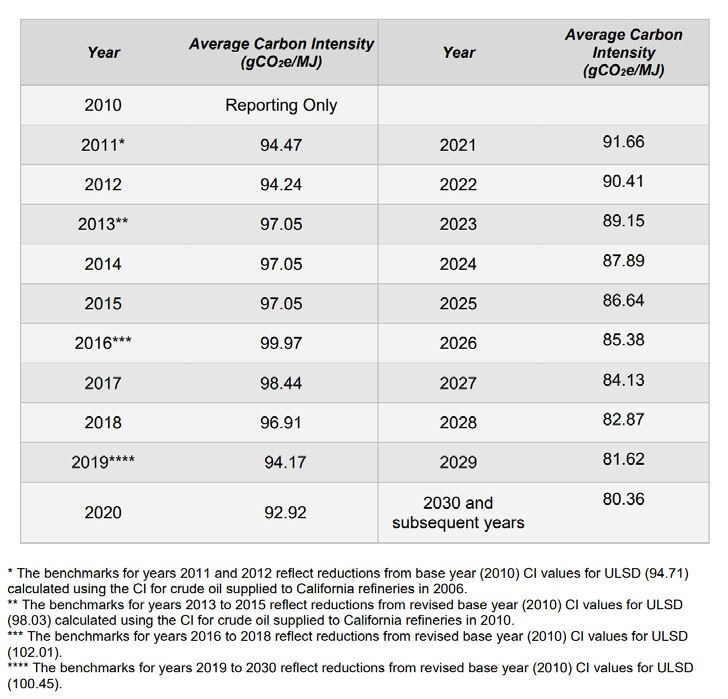

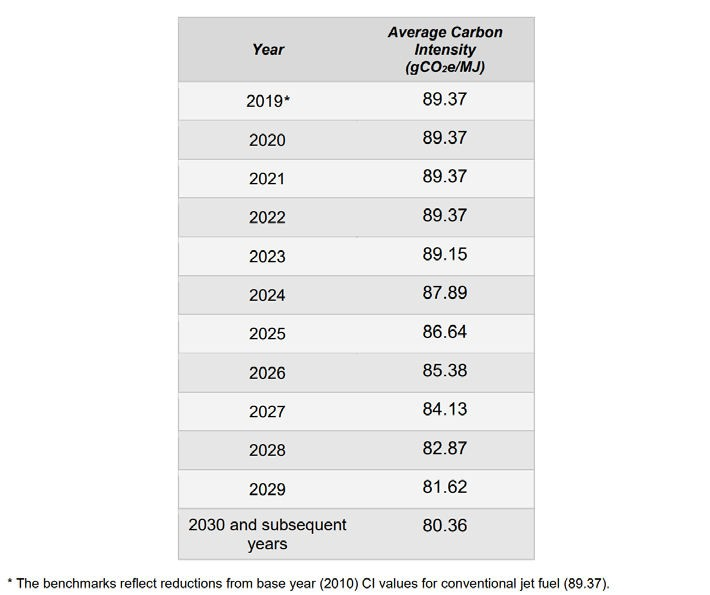

The annual California CI benchmarks through 2030 and beyond can be found in Table 2 and Table 3 below, copied from the CARB website effective July 2020.

Table 2: California LCFS CI Benchmarks for Gasoline

LCFS Carbon Intensity Benchmarks for 2011 to 2030 for Gasoline and Fuels Used as a Substitute for GasolineTable 3: California LCFS CI Benchmarks for Diesel

LCFS Carbon Intensity Benchmarks for 2011 to 2030 for Diesel Fuel and Fuels Used as a Substitute for Diesel Fuel

Conventional Jet fuel is currently an exemption to the LCFS program and does not generate deficit to the transportation fuel pool. However, CI benchmarks are established by CARB to determine the credits that can be generated for alternative jet fuel producers.

Table 4: California LCFS CI Benchmarks for Jet Fuel

LCFS Carbon Intensity Benchmarks for 2019 to 2030 for Fuels Used as a Substitute for Conventional Jet Fuel

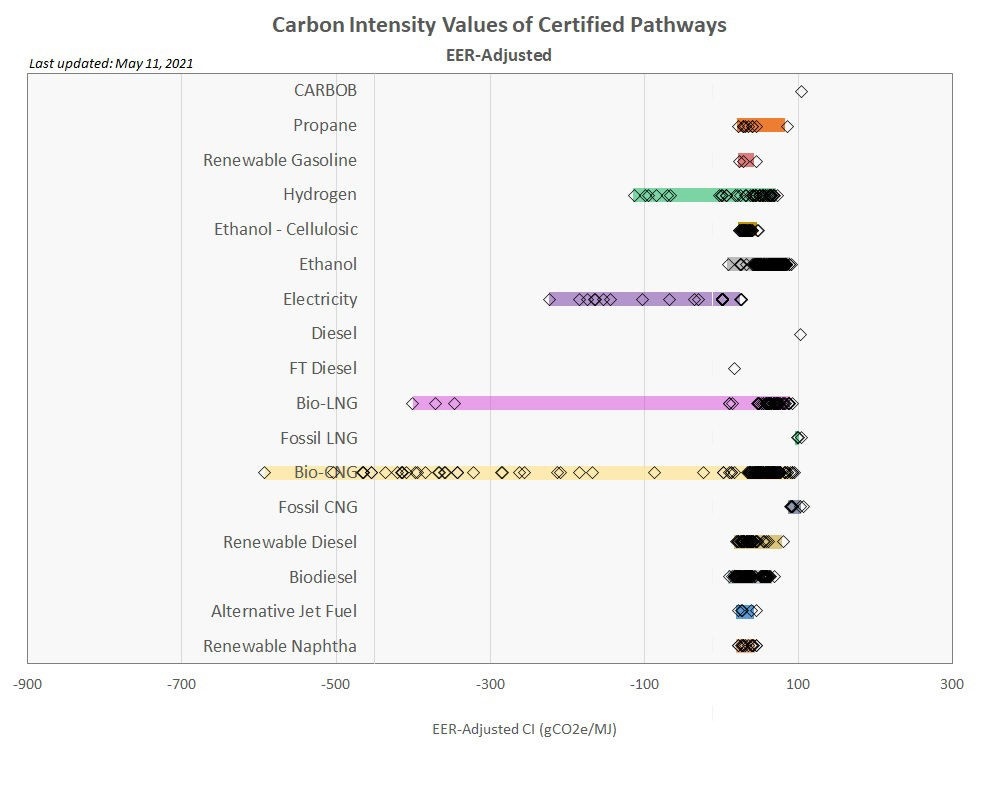

CARB may update the CI score of California fuels periodically based on energy and emission updates along the life cycle pathway. California gasoline and diesel produced from the average efficiencies of California refineries are 100.82 and 100.45 gCO2e/MJ respectively as of 2020. CARB also assigns each alternative fuel an Energy Economy Ratio (EER). An alternative fuel’s CI score divided by its EER results in the EER adjusted CI score, which represents emissions produced from the alternative fuel per MJ of conventional fuel displaced. Refer to Table 5 below for established lookup table by CARB19 and Figure 7 for various EER-adjusted CI scores of common alternative fuels.

Table 5: Lookup Table for Gasoline and Diesel and Fuels that Substitute for Gasoline and Diesel

CARBOB - based on the average crude oil supplied to California refineries and average California refinery efficiencies

100.82

Diesel

ULSD

ULSD - based on the average crude oil supplied to California refineries and average California refinery efficiencies

100.45

Compressed Natural Gas

CNGF

Compressed Natural Gas from Pipeline Average North American Fossil Natural Gas

79.21

Propane

PRPF

Fossil LPG from crude oil refining and natural gas processing used as a transport fuel

83.19

Electricity

ELCG

California average grid electricity used as a transportation fuel in California

93.75 (and subject to annual updates)

ELCR

Electricity that is generated from 100 percent zero-CI sources used as a transportation fuel in California

0.00

ELCT

Electricity supplied under the smart charging or smart electrolysis provision

Refer to CARB Current Regulation

Hydrogen

HYF

Compressed H2 produced in California from central SMR of North American fossil-based NG

117.67

HYFL

Liquefied H2 produced in California from central SMR of North American fossil-based NG

150.94

HYB

Compressed H2 produced in California from central SMR of biomethane (renewable feedstock) from North American landfills

99.48

HYBL

Liquefied H2 produced in California from central SMR of biomethane (renewable feedstock) from North American landfills

129.09

HYEG

Compressed H2 produced in California from electrolysis using California average grid electricity

164.46

HYER

Compressed H2 produced in California from electrolysis using zero-CI electricity

10.51

Figure 7: EER-adjusted CI Values of Certified Pathways

(See LCFS Pathway Certified Carbon Intensities website for up-to-date information)

Note that gasoline (CARBOB) and diesel benchmarks are included for reference alongside the EER-Adjusted CI values shown in Figure 7. Additionally, the length of each bar represents the possible range of CI value for the particular pathway, depending on the full emissions lifecycle of the fuel.

An example deficit calculation for 2020: a California refiner is subject to gasoline and diesel deficits on the order of 100.82 – 91.98 = 8.84 gCO2e/MJ for CARBOB gasoline and 100.45 – 92.92 = 7.53 gCO2e/MJ for ULSD. The impact to refiners in this deficit position is economics. The larger the spread of the CI fuel produced and the benchmark, the larger the credit deficit position.

The price of an LCFS credit hovered just below $200/MT (metric ton) at the end of Q1 2021. Current prices of an LCFS credit can be found on the CARB website, and a weekly snapshot as of end of April 2021 is shown in Table 6 below.

Table 6: LCFS Credit $/MT of CO2

LCFS Weekly Snapshot

Fuel Pathway Code

Transfer Type

All Non Zero

Type 1

Average Price (1) ($/MT)

$190

$175

Price Range ($/MT)

$168 - $213

$168 - $193

Total Volume (MT)

470,789

214,909

Total Value ($)

$89,353,572

$37,506,772

Notes:

Volume weighted average

There are three ways to generate credits in the LCFS program. To be clear, these options are for generating credits and doesn’t lower the deficit position implied annually. The capital costs involved to create these credit generating assets can be considered by refiners in deficit positions to reduce the amount of credit purchasing.

Fuel Pathway-based Crediting – All transportation fuels need a carbon intensity score to participate in the LCFS to generate credits, and the fuel type dictates which process is used to determine that CI. This option will be the most capital-intensive for a petroleum refiner. This is essentially only an option when considering a new renewable feedstock to either replace the petroleum feed or co-process, as this constitutes a new fuel pathway with a lower CI score. Being a petroleum refiner will still be in a deficit position, but a co generation of renewable fuels will generate credits.

Project-based Crediting – Projects include actions to reduce GHG emissions in the petroleum supply chain. This may include innovative crude – crude oil produced using methods like solar-generated electricity, refinery investment credits, renewable hydrogen used in refining, and carbon capture and sequestration (CCS) using direct air capture. Crediting for projects is based on life cycle emission reductions and credits are issued after the reported reductions are verified. This option can be leveraged to replace utility usage such as electricity and hydrogen from high CI sources to low CI sources. There are currently projects in California Kern county that are installing photovoltaic solar panels and battery storage to replace the electricity usage by oil refineries. For electricity, this reduces the GHG emissions from the grid source of 93.75 gCO2e/MJ to 100% zero-CI source solar electricity of 0 gCO2e/MJ. These projects are economically viable with the government credits and are a way of reducing the carbon intensity of existing facilities and essentially partially electrifying the existing fuel system and fleet.

Zero Emission Vehicle (ZEV) infrastructure (Capacity-based) Crediting – Introduced in 2018, crediting for ZEV infrastructure is based on the capacity of the hydrogen station or electric vehicle (EV) fast charging station less the actual fuel dispensed. This option is an “infrastructure credit” aimed at promoting building out ZEV infrastructure while providing an incentive to receive credits.

Applying for any of the above crediting programs requires registering the facility with CARB. There are essentially two main portals used to participate in the LCFS program and can be found on the CARB website.

LCFS Reporting Tool (LRT) and Credit Bank & Transfer System (CBTS). This portal serves the function of credit management system and annual reporting.

Alternative Fuel Portal (AFP). This portal serves the function of alternative fuel registration and CI pathway application & evaluation process.

The process of applying for a renewable CI fuel pathway and being certified for generating credits can be broken down into three categories, which essentially depend on the adoption level of the technology and CARB board experience in evaluating the process pathway. The full list of requirements for each of these categories can be found on the CARB website under the current regulation.

Look up table pathway applications is the simplest of the three and is limited to conventional fuels and simple electricity and hydrogen generation.

Tier 1 pathway applications involve processes that are more rigorous than the above, but the technology is generally industry adopted and CARB board has experience in evaluating the technology.

Tier 2 pathway applications involve processes that are upcoming technologies, and the CARB board has limited experience in evaluating. More rigorous review and documentation is generally associated with this pathway.

Tier 1 and 2 pathway applications require a life cycle analysis of the transportation fuel, which employs the use of the Argonne National Laboratory Greenhouse gases, Regulated Emissions, and Energy use in Technologies model (GREET model). This is a rigorous analytical tool that simulates the energy use and emissions output of various vehicle and fuel combinations. This analytical tool can be used to determine a refiner’s overall CI score of the transportation fuels and potential reductions in CI score for implementing renewable fuels into the transportation fuel pool.

The demand for transportation renewable fuel in the United States is mainly driven by policies as mentioned above per the RFS and LCFS programs. The RFS program drives renewable fuels production based on a volume mandate and incentivizes producers around the nation to generate valuable RIN credits as supply for regulated parties to purchase. On the same notion, the LCFS program drives renewable fuels and energy usage based on a carbon mandate and incentivizes zero emission sources using the CI score.

In the U.S., the RFS RIN program requires that refiners and importers of gasoline and diesel fulfill a renewable volume obligation (RVO). Entities within the U.S., as well as foreign entities, may be able to participate in the RFS RIN program by producing renewable fuel to blend and/or generate credits to sell so that obligated parties can fulfill their RVO requirements to meet compliance. The program mandates obligated parties to a required RVO annually, and they must either incorporate renewable fuel and generate RIN internally or purchase RIN on the market.

The Renewable Fuels Association reports that some refiners did in fact take steps to increase their renewable fuel blending capacity and capture RINs internally. Meanwhile, other refiners refused to invest in biofuel blending capacity, choosing instead to purchase RINs from parties who blended more than required.

The RVO to regulated parties will increase annually per the RFS EPA Volumes that can be found on the EPA website. The deficit incurred by obligated parties is set to increase until 2023 and possibly beyond 2023 subject to EPA’s decision.

In the U.S., the market for carbon credit programs is currently limited to California and Oregon. Other states are considering the LCFS program, which can open up the market for incentivizing more credit demand. Additionally, Canada is planned to have a nationwide Clean Fuel Standard in effect by end of 2022 which will open up a large market. Producers of credits outside of these carbon mandated states can opt into the program and sell valuable credits for regulated parties within these mandated states.

“Stillwater estimates that nearly 75% of all credits generated in both states [California and Oregon] are from fuels brought in from other states or countries. The value of these credits from fuels produced out-of-state in 2019 was more than $2.1 billion in California and nearly $140 million in Oregon.”

The U.S. government and armed forces are using a wide range of renewable fuels and has continued interest in exploring new technologies and different types of renewable fuels, but there is minimal use of renewable fuels due to availability.

The U.S. Navy's objective is centered around energy security, energy efficiency, and sustainability while remaining a power on the seas. In 2014, renewable fuels were included in the U.S. Navy’s fuel procurement request for the first time in history. The U.S. Navy's interest in renewable fuels was part of its goal to generate 50% of its energy from alternative sources by 2020. In particular, the Navy’s interest is in renewable fuels that can be used as direct replacements for petroleum-based gasoline and distillate fuels, also known as drop-in biofuels. The Navy also sailed the Great Green Fleet in 2016 to demonstrate the sea service’s efforts to transform its energy use. Deployed on alternative fuels, this fleet brought awareness to the Navy’s initiative to usher in the next generation of energy innovation. The Great Green Fleet was fueled by nuclear power for the carrier and a blend of renewable fuel made from beef fat and traditional petroleum.

The U.S. Air Force uses over 2.4 billion gallons of jet fuel annually (0.16 million BPCD as compared to total U.S. commercial airline demand of 1.2 million BPCD) and they are the largest energy consumer in the Department of Defense. Since 2012, the Air Force had approximately 256 renewable energy projects, but appears limited to installation of near zero emission electricity generation. The projects include solar, wind, geothermal, and waste to energy. With a 1.2 million BPCD of annual commercial jet fuel consumption, a government mandate in the jet fuel industry would further drive the demand for renewable fuels in addition to the current diesel and gasoline renewable fuels.

In theory, any carbon-based biological material from a renewable source can be a feedstock for the renewable fuels market. In reality, not all renewable feedstocks can be processed equally. Currently, the most easily processed feedstocks in the renewable fuel markets are from vegetable and seed oils, animal fats, and other used oils. Vegetable and fatty acid oils are polar compounds and typical non-polar petroleum thermodynamic predictions are not applicable. More importantly, all of these feedstocks contain glycerol (an organic compound in the alcohol family with 3 hydroxyl groups) or glycerides (an ester formed from the reaction of one or more of the glycerol hydroxyl groups with a fatty acid chain). The fatty acid chain(s) on the glyceride may be either unsaturated or saturated and results in a predictable chemical profile for refiners to process. Products from the hydrotreating of the renewable oils are linear hydrocarbons which conform to standard non-polar petroleum thermodynamics.

Feedstocks such as yard waste or other woody plant material contain cellulosic content that provides structure to plants (cellulose, hemicellulose, or lignin). These are more difficult to process and have much lower yields than the glyceride-based biomass. In this case, producing any biofuel requires a two step process, first to break down the rigid outer structure of the plant cell wall, then upgrading to finished product.20 The deconstruction step can be achieved by way of pyrolysis, gasification, or by use of enzymes or catalysts.

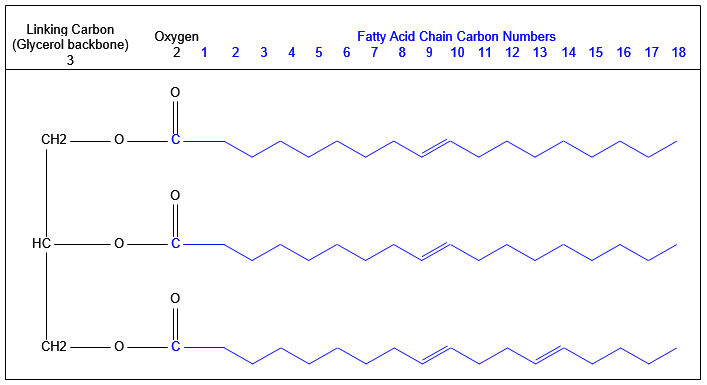

The quality of vegetable, seed, and fatty acid oil based feeds is remarkably consistent due to the glyceride content of each. While all glycerides contain the glycerol backbone, mono-, di-, and triglycerides are defined by the number of fatty acid chains on the ester groups. The fatty acid chains on the glycerides are defined by carbon number and olefin number, XX:Y. For example, lauric or dodecanoic has 12 carbons and no olefins, 12:00. Oleic or cis-9-octadecenic has 18 carbons and one olefin bond per chain, 18:01. A triglyceride consists of three fatty acid chains with each chain having the carbon number shown in the formula.

The molecular weight (MW) of triglycerides is high, 800 to 900, many with boiling points >1,000°F (538°C). On the other hand, the single chain fatty acids have MWs of 200 to 250.21 The molecular weight is calculated by understanding the molecular structure of each of the glycerides. Each glyceride is a unique molecular composition of repeating chains. The MW of individual glycerides of composition XX:Y is calculated by carbon number.21 The glycerides are a series of increasing carbon numbers and chain combinations. For example, corn has three glyceride chains each typically consisting of 54 w% linoleic, 28 w% oleic,13 w% palmitic, 2 w% steric, and 3 w% others. The chains are linked together by 3 carbons, 5 hydrogens. The calculated MW of corn ranges between 865 to 880 depending on the concentration of the glyceride distribution. The average corn molecular structure is shown in Figure 8 below:

Figure 8: Average Corn Molecular Structure

Typical value used for design; actual values may vary

Renewable feeds are primarily comprised of carbon, hydrogen, and oxygen. Sulfur and nitrogen contents are not routinely reported and are believed to be low < 100 wppm for vegetable oils and potentially higher for animal fats and waste cooking oil. The elemental analysis reported for the above feeds was calculated using the glycerides distribution and the carbon/hydrogen/oxygen composition of each. Because diesel specification does not set an initial boiling temperature, renewable diesel can accommodate the entire boiling point range for the fatty acid carbon chains noted in the glycerides distribution shown in Table 7 above, making it an ideal liquid fuels product for these feedstocks. Methods have been developed for calculating the thermodynamic and other properties required for design.

Virgin vegetable oil feedstocks provide a more consistent feedstock versus used cooking oil, which will have greater variation in contaminants. Vegetables have high concentrations of unsaturated fatty acids such as linolenic (18:03), linoleic (18:02), and oleic (18:01), whereas animal fats have more saturated fatty acids than vegetable oils, such as stearic (18:00) and palmitic (16:00). This has implication with respect to processing requirements for conversion to fuels. In general, more preprocessing will be required for higher contaminant feedstocks. Higher concentrations of unsaturated fatty acids will have higher hydrogen consumption for processing when compared to feedstocks with lower fatty acid content. Consideration of feedstock pretreatment should be a major focus of any renewable project.

Soybean is the largest source of biomass based diesel in the U.S., whereas rapeseed provides the lion’s share of feedstock for the rest of the world.27 The primary driver for the high use of soy in the U.S. is the need for protein meal for livestock. The protein meal’s coproduct soybean oil is sold as renewable feedstock. Unsurprisingly, the share of soybean oil utilized for biodiesel and renewable diesel in the U.S. has been steadily increasing over the years, reaching about 30% of total domestic soybean oil consumption of approximately 23-24 billion pounds consumed in 2018.28 With demand for both livestock feed and renewable fuels expected to increase in the next decade, soy planting is expected to rise accordingly, resulting in a continued source of soybean oil for renewable diesel feedstock in the United States.29 According to the U.S. Energy Information Administration (EIA), renewable diesel production capacity in the U.S. is on the order of 400 million gallons per year (26 thousand BPCD or 124 m3/m), U.S. renewable diesel consumption was over 900 million gallons in 2019 (21 million barrels or 3.4 million m3), and total diesel consumption in the U.S. (conventional and renewable) was about 47 billion gallons in 2019. Combined with the rising demand for renewable fuels, and increasing production capacity, it is likely that the demand for soybean oil and other renewable feedstocks may outpace the supply.

The future of renewable feedstocks largely focuses on non-food sources that are high in oil content, though emerging technologies are looking to expand the feedstock sources to include plant matter with lower oil content. The list of potential future feedstocks as of early 2021 is long, including microalgae, macroalgae, wood pulp, and others, which are generally classified as dry or wet feedstocks. From the U.S. perspective, considerable investment has been focused on algal biomass. The Department of Energy (DOE) estimates that the U.S. can produce 104-235 million metric tons of algal biomass and can do so sustainably and economically. In turn, this could yield 10-27 billion gasoline gallon equivalents (GGE) of algal biofuels annually, assuming productivity and fuel yield targets are achieved.30 GGE is a measure of how much alternative fuel is required to give the equivalent energy content of one gallon of conventional gasoline. The DOE’s Bioenergy Technologies Office (BETO) has targeted $3 per GGE pricing on technologies by 2022 and $2.5 per GGE by 2030.31

From a cultivation standpoint, microalgae are a potential source for renewable fuels; however, the technology has significant hurdles to make it economically feasible. On the plus side, algae have a high oil level and farming it does not require arable land. However, in addition to harvesting and transport logistics which require consideration, the product fuels depend heavily on the composition of the algal biomass, which in turn varies based on the type of algae, the nutrients they consume, and the environment in which they are grown. Various U.S. federal agencies such as the DOE, USDA, NOAA, and NSF are invested in researching increased algal biomass productivity and product yield.30

Perhaps the biggest hurdle for microalgae as a viable biofuels feedstock is the amount of nitrogen and phosphorus required for sufficient algae production. The amount of fertilizer required to meet a mere 5% of U.S. fuel demand would amount to more than double what’s used domestically to grow food.32 Since fertilizer components (nitrogen, phosphorous, and potassium mainly) are undesirable in finished fuels, they are generally removed by the refining process. The current focus on recycling these nutrients means the algae feedstocks of the future would require only a fraction of the fertilizer that conventional wisdom tends to quote. In addition, marine macroalgae would not require any man-made fertilizers.

The rapid growth rate (2-3 ft or 0.6-0.9 m per day) of marine macroalgae, commonly referred to as kelp or seaweed, and relative ease of cultivation as compared to microalgae may result in an overall lower production cost per barrel of biocrude produced despite lower yield results from preliminary studies. Biocrude is a mixture of hydrocarbons, fatty acids, esters, phenolics, and oxygenates that results from the conversion of biomass via chemical processes to liquid biofuel. Though the term is sometimes specific to the liquefaction process products, it is often used interchangeably with bio-oil, which is more often associated with the product of biomass pyrolysis. Marine macroalgae requires no fertilization, as cold ocean water provides the nutrients required for growth. The west coast of the United States in particular is well suited for macroalgae cultivation, as water conditions suitable for growth exist from Alaska to Southern California.33 While most of the global aquaculture production for macroalgae occurs in Asian waters,34 the United States has recently invested in research into offshore macroalgae production.

Several technologies are in development for converting biomass to renewable fuels. The DOE’s BETO office has placed emphasis on technologies that can process or co-process multiple different feedstocks to ensure a continuous source of biofuels. This minimizes the impact of variables such as growing seasons. Besides hydroprocessing of biomass to make renewable diesel, other technologies for the production of various biofuels include systems that require dry feedstocks (pyrolysis, gasification, trans-esterification) and systems that utilize the wet feedstock (hydrothermal liquefaction, fermentation, anaerobic digestion).35 Whichever method is utilized, post processing of the biofuel product is likely required. For instance, continuous hydrothermal liquefaction has been advanced to pilot-scale by the Pacific Northwest National Laboratory,36 and has been shown to produce biocrudes for both micro and macroalgal feedstocks. The biocrude product is high in nitrogen and Total Acid Number (TAN),37 which is logical considering the feedstocks require nitrogen for growth (fertilizer). Work in these areas is evolving rapidly and they could become future renewable energy feedstock sources.

Waste plastics can also be converted into energy. Incineration of waste can be used to produce heat and steam to power turbines which can generate electricity. In 2019, the U.S. burned 12.5% of its waste to produce electricity. This does nothing to reduce GHG emissions, since CO2 is produced. Byproducts of combustion also include toxic pollutants such as dioxins, acid gases, and heavy metals, which have their own pollution control methods for mitigation.

Gasification can also be used to recycle waste plastic. The polymers in plastics are decomposed into smaller hydrocarbons which can be used as fuels or raw materials for other petrochemical products. Since gasification is done in the absence of oxygen, dioxins and furans are not formed.

Plastic pyrolysis may also be used to convert waste plastic into energy. Under the proper temperature in the absence of oxygen, the polymers can be decomposed into gasoline and diesel boiling range materials. Catalysts may also be used in the pyrolysis equipment to optimize the fuels.

Since the plastics are made from fossil fuels and the final product is CO2, it is debatable whether or not energy from plastic waste can be considered renewable. As of 2019, 16 states considered municipal solid waste as a renewable fuel source.38

On a pure volume basis, by far the largest renewable fuel stock in the United States is the ethanol that is blended into the gasoline pool. Roughly 40% of the United States corn production is converted into ethanol for gasoline,39 which is associated with a fuel ethanol production capacity of roughly 1.1 million barrels per day (17.3 billion gallons/year or 5.4 million m3/month) in the U.S. as of January 2020. Even with so much current focus on renewable distillate fuels, U.S. production capacity of biodiesel and renewable diesel lags behind at roughly 164,000 barrels per day (2.5 billion gallons/year or 793,000 m3/month) of biodiesel in 2020 and 26,000 barrels per day (400 million gallons/year or 126,000 m3/month) of renewable diesel in 2018. Further, renewable gasoline production volumes sourced from entirely renewable feedstocks are less than comparably sourced renewable diesel volumes. This is likely due to a combination of factors such as ease of conversion (renewable diesel feedstocks such as soybean oil are already in the diesel boiling range), economic incentives, fuel demand opportunity, and the already renewable ethanol component of conventional gasoline found at the pump. In the U.S. RFS program, the renewable fuels category D6 RINs (which is exclusively ethanol) is the largest volume requirement, larger than the other fuel category D3/D7, D4, and D5 RINs. Coupled with the 1990 Clean Air Act, reformulated gasoline essentially exclusively uses ethanol as an oxygenate. Most of the gasoline sold in the U.S. contains ethanol up to the maximum 10% blend volume.

Government programs (both EPA RFS and California LCFS) are set up so that credit opportunity exists for renewable gasoline production. As of 2021, the RFS program includes approved pathways for producing renewable gasoline from cellulosic feedstock and renewable naphtha from limited plant oil feedstock, such as distillers corn oil and distillers sorghum oil. The California LCFS program is set up such that lower carbon intensity pathways generate more credit. That means a process producing renewable gasoline with a low CI score from all forms of technology may be considered for credit generation.

The renewable fuels industry has shown much interest in renewable gasoline in different forms of production. Studies have been conducted for using a Fluid Catalytic Cracker (FCC) to take feed of plant oils or co-processing pyrolysis oil with vacuum gas oil, allowing for re-use of a refinery asset for renewable gasoline production. Projects with Fisher-Tropsch technology are currently in operation, in construction, and planned for future construction. Shell’s Pearl gas-to-liquids plant in Qatar was built and operating since 2011, while Nacero announced in Q2 2021 that they are planning a gas-to-liquids plant in Texas using several other technologies to reduce carbon footprint.

Some momentum has started for 100% renewable gasoline into commercialization as of 2021, but is dwarfed by the current government program for ethanol production. The future of commercialized mass renewable gasoline production may depend on government incentives beyond that of the existing RFS.

Ethanol has been a major fuel constituent in the transportation fuels sector dating back to the 1970s. Most of the gasoline sold in the U.S. is blended with some amount of fuel ethanol, with E10 gasoline blend being the most common. The ethanol use in gasoline blending was significantly boosted by both the EPA RFG and RFS program starting in the early 2000s. The goal of the EPA RFG program was to achieve cleaner burning gasoline with oxygenates, while the EPA RFS goal is to increase renewable fuel use. By 2011, most gasoline-powered engine in the U.S. could use E10 gasoline, but higher ethanol blends result in significant decreased fuel economy. This is mainly due to the energy content of ethanol having 67% of the energy content of gasoline. The tradeoff of E10 gasoline is a slight decrease of about 3% in fuel economy while achieving cleaner burning fuel and sourcing from renewable. Additionally, only specific types of vehicles can use gasoline blends higher than 10% due to corrosion issues at high ethanol content.

While synthetic (non-renewable) ethanol exists, the vast majority of ethanol is sourced from a variety of agricultural feedstocks, primarily corn in the U.S. and sugarcane or sugarbeets elsewhere in the world40 and is thus considered a renewable fuel additive. Ethanol from renewable sources has been mainly driven by the RFS program. Recall that the RFS program requires a minimum amount of renewable fuels to be blended into transportation fuels, with that minimum increasing each year. Ethanol is an obvious choice to meet this requirement due to its high octane properties and renewable feedstock sources. The RFS plan was based on the idea that as gasoline consumption increased alongside the increasing minimum renewables requirement, the national fuel supply could stay at or below the E10 blend wall, or the maximum ethanol blend to avoid engine or fuel system damage in vehicles not designed for fuel past E10 grade,41 which includes most vehicles on the road today. EPA suggests that gasoline consumption in recent years has been close to the E10 blend wall level. From 2015 through 2019, fuel ethanol consumption equaled about 10% of total U.S. motor gasoline consumption.

As gasoline consumption is likely to decline as a result of increasing remote work options and increasing popularity of electric vehicles, the U.S. is on track to hit the ethanol blend wall. Possible solutions to the blend wall problem include adjusting the RFS rules, which would require a change to government regulations, changes to the way engines and fuel systems are made, increased production of E15 and E85 gasoline, neither of which helps cars already on the road, or finding another renewable oxygenate to use instead of ethanol.

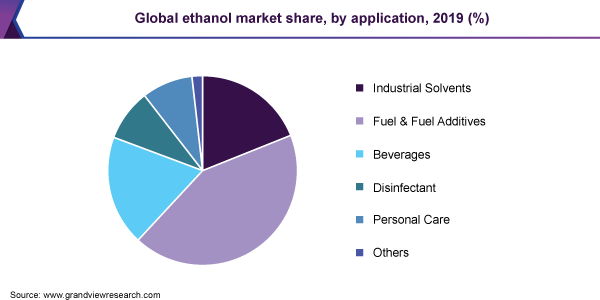

In a future scenario where electric vehicles make up automotive market share and market demand for gasoline declines, the use of ethanol in gasoline would also decline as a majority of ethanol used today is for the purpose of blending into gasoline. In 2019, ethanol use in fuel & fuel additives had a market share of approximately 43% (see Figure 9). There remains opportunity for ethanol and ethanol producers to shift assets into relevant markets in fuel and chemicals.

Figure 9: 2019 Global Ethanol Market Share

The demand for gasoline as a transportation fuel is seen on a path of decline with increasing policies and interest to adopt zero emission vehicle (ZEV) powertrains. This decline in gasoline demand is expected to be seen in the near-term, affecting light and medium-duty vehicles. While the U.S. has some states that have adopted ZEV and low-emission vehicle regulations, no federal legislation is currently in place. However, California has recently announced executive orders that will aggressively push the market into ZEV. California will require all new passenger cars and trucks sold in the state to be emission free by 2035. In addition, California will also require all semi-trucks sold in the state to be emission free by 2045.

Ethanol producing plants may face business decisions in a changing market where ethanol demand in gasoline diminishes. This leaves ethanol producers to consider unconventional market opportunities such as other transportation fuels or chemicals. As light and medium duty passenger vehicles are the primary focus of ZEV powertrains, ethanol could be a feedstock to produce renewable diesel and SAF while capturing government incentive programs in transportation fuel. There are several companies that recognize this opportunity in the current market landscape and have positioned themselves as technology owners.

Gevo, a Colorado based company, has a commercial facility making isobutanol alongside ethanol and produces it using a genetically modified yeast. They have also been producing alcohol-to-jet (ATJ) derived from isobutanol since 2011 at South Hampton Resources located in Silsbee, TX. Gevo’s ATJ fuel was used in certification tests, including test flights with the U.S. Air Force, U.S. Army, and U.S. Navy. Since receiving its ASTM certification in 2016, Gevo’s ATJ fuel has been used in commercial flights around the world and working towards commercialization.

Vertimass, a California based company, is developing a proprietary catalyst for converting ethanol into renewable diesel, SAF, and renewable chemicals. As of 2017 they have several pilot plants as proof-of-concept and continuing improvements and development with a target to commercialization.

Other opportunity exists in the chemical industry. Axens has a dehydration technology of converting renewable ethanol into bio-ethylene. The bio-ethylene produced can be integrated in existing downstream polymerization installations such as polyethylene (PE), polystyrene (PS), polyethyleneteraphthalate (PET), polyvinylchloride (PVC) and acrylonitrile- butadiene-styrene (ABS) without need for modifications.

Zero emission vehicles (ZEV) have proven to be a reliable alternative to the internal combustion engine in today’s market. Electric motor vehicles have taken the center stage as the alternative powertrain technology. Electric battery packs as the source of energy are on a path to price parity with internal combustion engine cars. The near-term expectation of light and medium-duty transportation vehicles is a shift to zero emission vehicles. This would lead to the decline of demand in gasoline fuel as more ZEVs are adopted. However, as discussed above, today’s electricity is largely generated from fossil fuel sources. Until the grid has turned over to be renewably sourced, renewable liquid fuels are a viable alternative for GHG reduction during the transition. Renewable liquid fuels are also the only pathway for the existing ICE fleet.

The current U.S. government mandates on renewable gasoline are limited to the RFS and LCFS programs. Even though ethanol blending began with the Clean Air Act for the purpose of reducing smog and harmful toxins, it is the RFS program that mandates blending 10% ethanol into conventional gasoline pool, which coincides with the program’s Renewable Volume Obligations (RVO) to refiners. Technology exists to produce renewable gasoline, and complies with the RFS program, but is not widely industry adopted as of 2021. The state level LCFS program mandates a carbon reduction via a credit market, putting lower carbon intensity score produced gasoline in favorable position for selling credits to deficit producers. This program is designed to incentivize lower intensity score renewable fuel processes. Ethanol producers can generate credits in this market to sell, but the program does not necessarily drive the mandate for ethanol nor any other type of sustainable process.

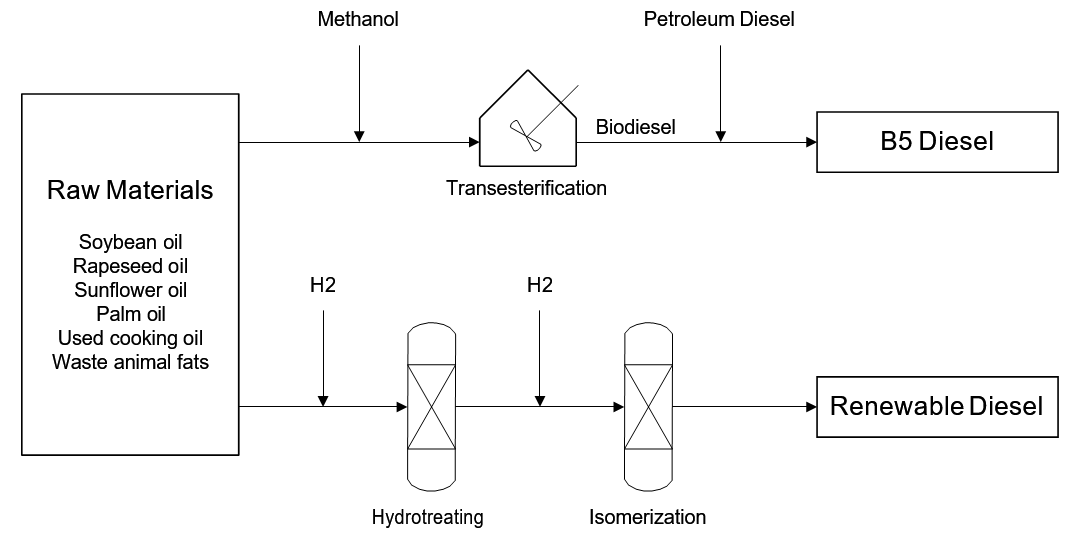

Biodiesel and renewable diesel are both made from renewable resources. However, they are not the same. Biodiesel is made by transesterification of a glyceride with an alcohol. 100% biodiesel cannot be used directly in unmodified vehicles because biodiesel retains the oxygen from the glyceride’s ester group after the transesterification process. Biodiesel is not chemically the same as conventional diesel, and does not meet diesel cold flow property specifications. Blending with petroleum-based diesel in mixtures up to 20% allows the biodiesel to meet engine fuel specifications. Renewable diesel is made by hydroprocessing of glycerides, producing a fuel that is fully fungible with conventional diesel, but is more expensive to produce.

Figure 10: Biodiesel and Renewable Fuels Production

Biodiesel is made by transesterification of glycerides found in the feedstock oils. The transesterification reaction is the process by which glycerides and alcohol – most commonly methanol – are converted into alkyl esters. The reaction is catalyzed by a strong acid or base. Industrial scale processes commonly use sodium or potassium methanolate.42 The products of transesterification of glycerides with methanol are fatty acid methyl ester (FAME), or biodiesel, and glycerol.

Biodiesel cannot be used directly in most vehicles and typically has to be blended with petroleum diesel. Up to 5% FAME (B5 biodiesel) is allowed by many vehicle manufacturers with some that can accommodate up to 20% FAME (B20 biodiesel). Biodiesel has different solvent properties from petroleum-based diesel. Impurities such as methanol, free fatty acids, water, catalyst and glycerol left in the biodiesel may increase corrosion,43 causing degradation of rubber gaskets and hoses in vehicles. The cold flow properties of biodiesel vary depending on the feedstock but are generally worse than both petroleum based and renewable diesel. These cold flow properties make biodiesel unusable in cold climates without blending with petroleum diesel or additives. Table 8 below shows a comparison of cold flow properties of biodiesel from various feedstocks and No. 2 petroleum diesel.44

Table 8: Biodiesel Cold Flow Properties

Soy

Canola

Lard

Edible Tallow

Inedible Tallow

LFFA (1) Yellow Grease

HFFA (2) Yellow Grease

#2 Diesel

Cloud Point, °F (°C)

36 (2)

27 (-3)

57 (14)

68 (20)

73 (23)

108 (42)

46 (8)

0 (-18)

CFPP, °F (°C)

28 (-2)

24 (-4)

52 (11)

58 (14)

50 (10)

52 (11)

34 (1)

-4 (-20)

Pour Point, °F (°C)

30 (-1)

25 (-4)

52 (11)

56 (13)

46 (8)

54 (12)

46 (8)

-17 (-27)

Kinematic Viscosity @40°C, cSt

4.55

4.63

4.85

4.91

4.93

5.62

4.66

2.45

Notes:

LFFA – Low Free Fatty Acid

HFFA – High Free Fatty Acid

The byproduct of biodiesel production by transesterification is glycerol. Glycerol can be used in the food and cosmetic industries. Anaerobic digestion of glycerol can also be used for methane production and power generation.

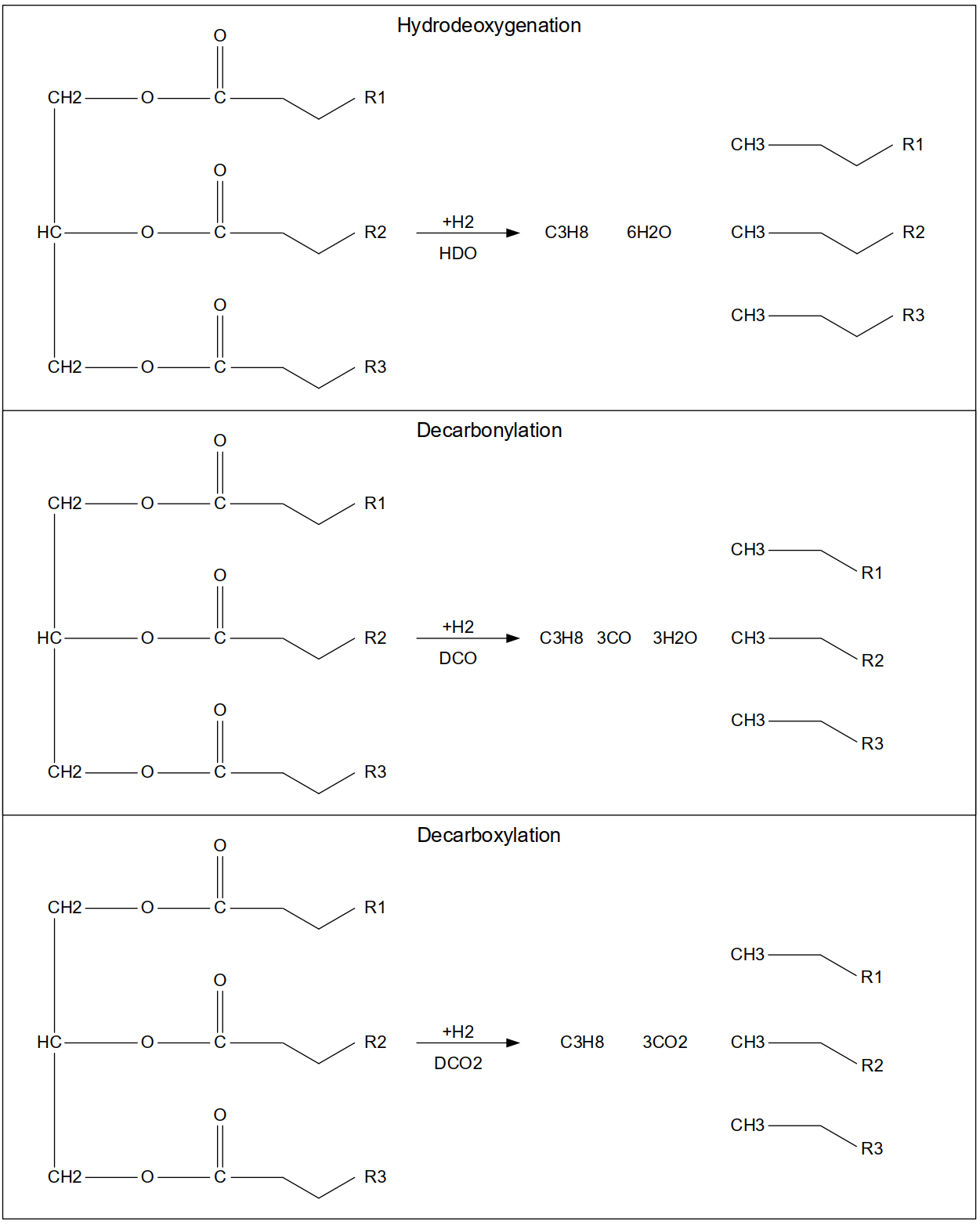

Renewable diesel uses the same raw materials as biodiesel but processing is by more typical refining processes. Feed glycerides are remarkably consistent between feeds with the difference being the concentration of individual carbon chains. The olefins in the glycerides are saturated and deoxygenated by adding hydrogen and processing over hydrotreating catalyst. The products of the hydrotreating reactions, including possible side reactions of reverse water gas shift and methanation, are straight chain paraffins, water, methane, propane, CO2, and CO. The water and gases are separated from the hydrotreating effluent. The paraffinic stream is sent to an isomerization reactor to improve cold flow properties. Additional details about the reactions can be found in the Reactions discussion under the Existing Refinery Retrofit section.

Yield of liquid fuel from the hydroprocessing of renewable feedstocks is reasonably good, roughly 75-80 wt%. Assuming a generic triglyceride with a carbon chain of 18 carbons, 1.2 olefin bonds per molecule, and an O2 content of the mixture at 11%, theoretical yields are estimated in Table 9 below.

Table 9: Biodiesel Cold Flow Properties

Generic Yields from the Chemistry Basis: the entering triglyceride as a wt%

Hydrogen consumption